READ TIME: 4 MIN

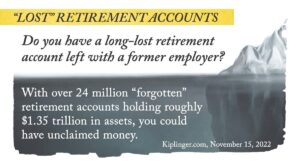

When you change jobs, it’s critical to remember to create a plan for past employer sponsored retirement accounts. While you have the choice to simply leave it, you also have the option to consolidate past plans which brings all funds into one account. Here are a few things to consider when deciding what to do with numerous retirement accounts:

IRA Benefits

Changing jobs opens up the option to consolidate your earned 401(k) funds into one account. Oftentimes consolidating previous plans into one account can reduce paperwork, make it easier to rebalance investments, monitor progress, plan a withdrawal strategy, and maintain beneficiaries. It also may reduce administrative fees, which can add up over time, especially when factoring compound interest. Consolidating can also qualify investors for breakpoints based on asset and trading thresholds.

It’s important to carefully consider the pros and cons of rolling former employer accounts into a personal IRA.

Advice & Planning Services

Often, 401(k) administrators won’t advise on investments or the suitability of a rollover. When making decisions on 401K Rollovers and the options available to you there are benefits to consulting with an Independent Financial Advisor.

1. They can work with you to develop a more holistic financial plan for you and your family. A plan that includes investing, lending, credit, budgeting, risk management and more.

2. The relationship is more responsive and personalized. They work closely with you not only to understand your current financial position, but what your goals are in order to make sure your financial decisions are in alignment with those goals.

3. Their continuing education, expertise and experience is available to you to support and assist you. Especially when the ups and downs of the market can trigger individuals to make emotional or rash decisions with their money.

Greater Investment Options

IRAs offer more control over the investments and more investment options. Typically, 401(k) plans include a few dozen funds to choose from, while IRAs offer thousands of investment choices. A rollover to an IRA allows you to reinvest your money in a wider variety of investment options, such as stocks, bonds and ETFs. It also provides you with flexibility in buying and selling your holdings without penalty whenever you want to rebalance your portfolio or change strategies.

Inheritance Options

IRA accounts can provide more freedom if a spouse passes away. Under federal law, surviving spouses automatically receive their deceased spouses’ 401(k)s – unless the survivor has signed a waiver. IRAs usually allow multiple or contingent beneficiaries. The SECURE Act eliminated “stretch” IRAs, which allowed children and grandchildren to take minimum distributions from an inherited IRA over their lifetimes. This has created the need for more nuanced estate planning strategies to reduce taxation and ensure your loved ones receive the maximum amount of inheritance.

Simpler Communications

Leaving your 401(k) with your previous employer may make it harder to contact an account admin or receive the latest account communications. Rolling multiple 401(k)s into one IRA reduces the complexity of juggling several workplace accounts and makes accessing information easier.

Decreased Fees and Costs

It’s common for employer-sponsored 401(k) plans to offer mutual funds that can impose higher management fees, which can add up over time. But the fees don’t necessarily make a 401(k) a bad deal: 401(k) contribution limits are three times higher than an IRA, plus you often receive an employer match. Those two benefits can outweigh the management fees you may encounter in a 401(k) fund lineup.

These are just some of the benefits of rolling over a 401(k) into an IRA. We specialize in helping households transition from working years to retirement, so contact us today to discuss the best rollover options for you!

401(k) Benefits

On the other hand, 401(k)s carry some unique benefits. They are protected from all types of creditor judgments. Traditional and Roth IRA assets up to a certain amount are shielded from bankruptcy claims. Creditor safeguards vary from state to state so it’s important to be aware of your individual state guidelines.

Another benefit of keeping funds in a 401(k) is if you leave your job after the age of 55, you can take penalty-free withdrawals from a 401(k) account. The minimum age for withdrawing from an IRA without a penalty is 59½.

You can take up to a five-year loan from a 401(k); whereas an IRA only affords a 60-day, tax-free rollover option.

Carefully consider potential fees and tax implications before consolidating. New Department of Labor Laws have made this process more transparent than ever. We now have software that can analyze your current plan as well as any of our recommendations to ensure you have all the information and as a fiduciary, we are acting in your best interest.

As you can see there are many considerations to take into account when you are thinking about rollover or consolidating a 401K. We are happy to help you decide if consolidating your accounts would be beneficial and to help you weigh advantages and disadvantages of rolling 401(k)s into a personal IRA. Please reach out with any questions you may have. As always, we are here to help!

Recent Comments